Seasonally adjusted unemployment rates for all Utah counties have been posted online here.

Each month, these rates are posted the Monday following the Unemployment Rate Update for Utah.

For more information about seasonally adjusted rates, read a DWS analysis here.

Next update scheduled for March 26th.

Showing posts with label Economist--Matt Schroeder. Show all posts

Showing posts with label Economist--Matt Schroeder. Show all posts

Monday, March 5, 2018

Monday, January 29, 2018

Ten Years Later:

Differing patters of recession and recovery in Bear River

December 2017 marked 10 years since the Great Recession

first cast its long shadow across the American economy. The recession

officially lasted 18 months, but its consequences can still be seen across the

country without having to look very hard. We have not had another recession

since.

Utah was hit hard at the time, losing a larger share of jobs

than the national average; but, we were fortunate to be one of the most

resilient states in terms of economic rebound. There are plenty of states where

the Great Recession continues to weigh upon them. Employment levels in 14

states are still not back to their pre-recession peak, and another 29 states

have only grown 5.0 percent or less. As the working-age population has grown by

more than 5.0 percent, the job gains nationally have not been enough to fully

employ working-age labor.

Utah lost 7.0 percent employment during the recession. Since

that low, employment has recovered by 18 percent. That is the second best

rebound in the nation. From Utah’s pre-recession employment peak to now, Utah’s

employment has increased by 9.5 percent, third best in the nation. Yet, Utah’s

job growth has not been enough to absorb all of the labor force growth during

that time. Utah’s unemployment rate is low, but the percent of the working-age

population in the labor force is several percentage points below the

pre-recession norm — telling us that potential labor is still not as fully

engaged with the job market as before the recession.

As a whole, Utah has had a notable recession rebound, but

those gains have not been shared equally across all regions. Just like the

national profile, some areas have bounced back strong while others are still

lagging behind. The state’s metropolitan areas have grown well, but many of

Utah’s rural areas cannot say the same. Nine counties have employment levels

below their pre-recession peaks.

In this issue of Local Insights, we profile Utah’s regional

and county economies in light of the 10-year span since the Great Recession.

Bear River Region

Although the three northernmost counties in Utah (Cache, Box

Elder and Rich) are often viewed as a single region, the reality is they each

have distinct economies and experienced differing recessionary impacts and recoveries.

For instance, Box Elder County is reliant on the manufacturing sector, which

was hit hard during the recession. Rich County is highly subject to swings in

tourism spending, which is among the first things consumers pull back on when

money is tight. Cache County, on the other hand, has a more diverse economy and

recession-resilient industries (like education) that help to mitigate the

severity of economic downturns.

Box Elder County

Just prior to the recession in 2008, the manufacturing

sector accounted for nearly 40 percent of Box Elder County’s total employment —

or about 8,100 workers. By 2012, that number had been slashed to around 4,500.

Layoffs at ATK Launch Systems and the La-Z-Boy closure slashed deep into the region’s

economic tissue. Although the initial ATK cuts were the end of NASA’s shuttle

program and not a direct result of recessionary pressures, the recession did

put budgetary constraints on the federal government leading to less money for

NASA and other types of contracts that might have kept ATK at higher employment

levels. In addition, the recession meant virtually no other jobs were available

and many people left the area. Net migration turned outward with about 500

leaving each year in 2011 and 2012.

Box Elder is only now getting back to its pre-recession employment

level of about 21,000. The good news is that since it turned the corner in

2013, growth has been robust — averaging more than 5.0 percent annually. Manufacturing

is still the primary driver of new growth; but within manufacturing, the

products being produced are more diverse. Motor vehicle parts, food and

fabricated metals now make up larger shares of manufacturing employment.

In addition to manufacturing’s resurgence and

diversification, other industries have begun to rise in economic importance

adding to the economy’s overall diversity and future recessionary resilience. For

example, health care services did not even dip during the recession and has

been on the rise since. Prior to the recession, heath care was about 6.0

percent of employment. Now it is up to 9.0 percent.

Rich County

Rich County lost about 150 jobs during the last recession — nearly

27 percent of its average employment. Only Piute County lost a larger

employment share. Tourism is the key to Rich County’s economy; and during

recessions, travel and recreation are among the first luxuries cut to pinch

pennies. Traveler accommodations alone shed more than half of its employment between

2007 and 2012 (from 90 to nearly 40).

Construction took a significant hit as well, shedding about

90 jobs over the same period. Most of the losses were in residential

construction with fewer vacation and retirement homes being built. In 2007,

there were 43 single-family homes permitted in Rich County. By 2012, that

number had dropped to just four.

Rich County’s recovery since late 2012 does not appear to be

driven by tourism spending. Some moderate growth in restaurants indicates

improvement in visitor spending, but the accommodations industry has basically

plateaued since the recession’s end. New single-family home construction is again

on the rise but has yet to return to pre-recession levels. Most of the recovery

growth is local business services, such as repair and maintenance, and building

services. Retail sales employment in lawn and garden, and building materials is

also a significant contributor to the recovery — indicating that local demand is

currently keeping Rich County on its growth trajectory. This is encouraging as

it suggests a shift away from tourism dependence and leaves room for even more

growth once travel spending resumes.

Cache County

Cache County did not contract nearly to the extent of Utah’s

other counties during the recession. It lost less than 800 jobs and contracted

only 1.6 percent. The downturn was short-lived too. The economy started expanding

again in early 2010, and regained its pre-recession employment by mid-2012 when

Box Elder and Rich counties were just bottoming out.

In Cache County there is no single sector that dominates the

local economy the way manufacturing does in Box Elder County. Manufacturing is

Cache County’s largest sector and comprises 19 percent of total employment.

And, most of Cache County’s manufacturing employment is in food manufacturing (especially

dairy and beef), which is highly recession-resilient. During recessions demand

falls for many nonessential goods and services; but core food products, such as

milk and meat, tend to hold steady. In fact, during the recession, employment

in both dairy and beef manufacturing actually grew and helped prop up Cache’s

economy.

Utah State University provided a similar stabilizing effect.

The university is the region’s core economic engine, accounting for about 12

percent of employment. Like food manufacturing, education services are not

prone to major recessionary setbacks. Historically, enrollment actually

increases when unemployment is high as more people who find themselves idle

choose to invest in education.

Cache County’s recovery has been steady and shared across

most industrial sectors. Growth at the university and the human and

intellectual capital it produces boost the vibrancy of other industries, as well.

Professional, scientific and technical services have been expanding employment;

as have medical services and even manufacturing industries, like chemical and

computer and electronic products. Such industry diversification will further

strengthen Cache County and its ability to weather the next recessionary

downturn.

Thursday, July 27, 2017

The New Retail Workforce:

How Online Sales are Changing Retail Jobs in Northern Utah.

Consumer spending makes up around 68 percent of the nation’s

gross domestic product. Consumer spending is individuals and families

purchasing groceries, clothing, recreation, stocks, insurance, education and

much more. The transactions cover a broad swath of economic activity.

Much of the nation’s consumer spending is captured via

retail trade. A useful retail trade definition is “the re-sale (sale without transformation) of new and used goods to the general public, for personal or household consumption or utilization.” Not all consumer spending is captured through retail trade transactions,

but a large share is.

Broad-category examples of retail trade sectors are motor

vehicle sales, furniture stores, electronic stores, building material stores,

grocery stores, pharmacies, gas stations, clothing stores and department

stores, among others.

Then there is the relatively new and emerging part of the

retail trade sphere — non-store retailers. These are establishments that sell

products on the Internet. Examples include Amazon, Zappos, Overstock.com, or

eBay. These types of retailers have grown rapidly in the past 15 years and

their presence is reshaping the retail trade landscape.

Whereas in the past nearly all retail transactions were done

through traditional brick-and-mortar stores, now a significant and growing

segment is diverted to internet sales. The consumer shops online and FedEx (or

like) delivers the product. One can see that the number of brick-and-mortar

stores and the level of local sales across the country are being endangered by

this economic evolution.

The brick-and-mortar reduction is beginning to show its

economic presence in the United States employment numbers. While the U.S.

economy is finally expanding at a healthy pace this side of the Great

Recession, one of the few industries not rising with this tide is retail trade.

While overall retail sales are increasing, employment is not.

Traditionally, as a population increases, retail trade

employment grows simultaneously, since population growth and consumer spending

volume is an integrated dynamic. If studied deeply, a certain ratio of retail trade

employment growth spawned from population growth would emerge. Before the

internet, the vast majority of all consumer sales occurred in the immediate

community or region. But now, the internet is diverting these sales away from

the local community — and with internet sales growing, its market share will

increase.

We do not yet know how much brick-and-mortar erosion will

eventually occur. And will such a phenomenon hit some areas more than others

(e.g., urban vs. rural, or local vs. tourist spending)? These are touch points

that economists will be watching as this internet sales phenomenon continues to

grow within the national and Utah economies.

In light of this change, in this quarter’s Local Insights we

are profiling retail trade employment throughout Utah’s local regions. This can

offer a profile of where retail trade is now in a local economy, and possibly

how much of the sector could become vulnerable to the internet-sales

phenomenon.

All regions can be viewed through the Local Insights

web

portal. The following is a retail trade profile for the Bear River region:

Retail Matters in the Bear River Region

The retail trade industry is an important economic driver in

Bear River. It employs more than 8,000 people in the region —almost 11 percent

of total nonfarm employment. In Box Elder County, retail trade is the third

largest industry, behind only manufacturing and health care. In Cache County,

it is the fourth largest. Retail sales account for about 51 percent of total

taxable sales in the region — very similar to the 52 percent statewide average.

The Rise of Online Retail

Due to consumers making more and more purchases online, the

demand for brick-and-mortar retail workers in the region has been softening.

Overall, employment in Bear River has been growing at a rate of about 2.4

percent on average since the recovery noticeably began in 2012; but in

traditional retail, employment growth has been averaging just 1.4 percent. In

the five years prior to the recession (and before online retail really took off),

traditional retail employment was clipping along at a much quicker average

growth rate of 2.6 percent growth.

Non-store retail, on the other hand, has been booming in the

region. With the growth of online retailers, like Malouf Linens and Jensen

Online Books in Cache County, employment in non-store retail has grown an

average of 16 percent annually since 2012. The share of total employment

represented by non-store retail has increased 105 percent over that time. The

next highest employment share expansion in retail was in the motor vehicles

category, which increased its share by a paltry 19 percent in comparison. Most

other retail categories saw a decline in their share of total employment.

Non-store Taxable Sales Are Also Gaining, But Not as Fast as

Employment. Why?

Taxable sales in non-store retail have not gained as a share

of total taxable sales as quickly as the employment share. This is primarily

because sales taxes are collected by the state of the purchaser, and then, only

if the seller has a physical presence in that state. This means that when

Malouf sells a pillow to someone outside of Utah, there is money coming into

Utah (in terms of the jobs that the sale supports) but there is no sales tax

coming in to Utah. The only non-store sales taxes captured in Utah are Utah

consumers purchasing goods from retailers with a presence in Utah. Since a

large share of sales by local online retailers are to customers in other

states, it means that sales tax revenue lags compared to employment growth in

the industry.

An Aging Retail Workforce

Interestingly, the jobs in retail are not primarily younger

workers as one might expect. In fact, about 70 percent of the region’s retail

jobs are people 25 and older, and approximately 45 percent are at least 35.

There used to be more young workers in the industry. Prior to the recession in

2007, the share of 35 and older retail workers in the Bear River Region was

only 38 percent.

During the Great Recession, the share of teenagers working

in retail plummeted from 9 percent to 4.5 percent and has remained low ever

since. The reduced youth base means there are fewer workers who stay on and age

into the older categories.

A Less Educated Retail Workforce

At the same time, the share of retail workers with less than

a high school education has increased significantly. This has been primarily at

the expense of individuals for whom educational attainment data are not

available (i.e., workers under the age of 24 — mostly students). Since 2007,

the share of workers with less than a high school education in Utah retail has

increased by more than 25 percent.

This does not appear to be an actual increase in less

educated workers. Rather, the drop in workers under 24-years-old is causing a

share increase for the existing less educated workers. As a result, the retail

workforce in Bear River (and in Utah in general) is trending toward an older

and less educated demographic.

What is Driving This Trend?

This is likely the result of young people choosing to take

jobs in other industries with better pay, as wages in retail have lagged. Or

they may be opting to finance their education rather than work while attending

school. But some portion of this shift is also being driven by the structural

changes taking place in retail due to increasing online sales.

The Occupational Shift

The transition to non-store retail translates to shifting

demand for a different set of occupations required by non-store retail

operations. Traditional brick-and-mortar retail stores primarily need people to

work on the sales floor, such as retail sales workers and cashiers. Those two

occupations alone represent about 45 percent of all employees in traditional

retail. In non-store retail, on the other hand, the top two occupations are

customer service reps and shipping/receiving clerks. Freight and inventory

movers, order clerks/fillers, and truck drivers all play a much more prominent

role in non-store retail as well.

Generally speaking, these kinds of jobs tend to require more

time commitment than the most demanded traditional retail jobs. According to the

Conference Board’s Help Wanted Online® product (analyzes online job postings),

about 40 percent of job openings for cashiers and retail sales workers (the top

jobs for traditional retail) posted in Utah in the second quarter of 2017 were

part-time jobs. Only 20 percent of job postings for customer service reps and

shipping/receiving clerks (the top jobs for non-store retail) were part-time.

Positions that require more time commitment and more fixed schedules are likely

to be less attractive to young people — especially students — who may be

looking for opportunities that are less time consuming.

The Geographic Shift

In addition, there is a geographic component to this

transition. Traditional retailers tend to have many more locations spread out

geographically, making them more likely to have that cover a broader footprint

within the labor force. Online retailers, however, are generally centralized in

large warehouses, distribution centers, and office buildings that runs counter

to the disperse spread of traditional brick-and-mortar. As a result, it may be

harder for workers — especially younger workers — to get to and from these

jobs.

What It All Means

These structural changes are having a profound effect on the

retail workforce, and we can reasonably expect the resulting trends to continue

for some time. As new technologies and retail processes emerge, there will

doubtless be more shifts in this rapidly evolving sector. But for now, in the

Bear River region, we can expect fewer traditional brick-and-mortar retail

jobs, more non-store retail jobs, and an increasing share of retail employment

opportunities that may be challenging for our young population to access.

Check Out the Viz

If you are interested in the details, the data visualization

below breaks out the various retail categories and allows you to compare sales

(as a share of total taxable sales) and employment (as a share of total nonfarm

employment) in each category (by county) over time. The relative changes in

taxable sales compared to employment are telling in relation to some of these

structural changes, although direct links are difficult to establish as there

are many other confounding factors. The tables at the bottom give the actual

sales and employment levels, summed-up for whatever you have selected in the

county and retail category filters.

Thursday, May 4, 2017

Census Bureau Tool Provides Labor-Force Insight for Bear River

Across the United States, jobs are quantified through each

state’s unemployment insurance program. Those programs provide the potential

for laid-off workers to receive unemployment benefits — the goal being to

bridge the gap between workers’ lost jobs and their next jobs. An eligible

recipient’s weekly benefit amount is based upon their earnings from recent

work. This begs the question, how does Utah’s unemployment insurance program

know how much an individual recently earned while working?

That answer is supplied by all businesses that hire workers,

as they must report their employees and pay as mandated by the unemployment

insurance laws. Companies identify their individual workers and those workers’

monetary earnings for a calendar quarter. As businesses are identified by their

industrial activity and geographic location, it is through the unemployment

insurance program that aggregate employment counts by industry and location are

calculated.

Yet each state’s profiling of individuals is quite minimal

in the unemployment insurance program. The U.S. Census Bureau can bring more

light to the overall labor force by supplementing said information with gender,

age, race/ethnicity and educational attainment (imputed from American

Community Survey responses) for Utah’s labor force.

The Census Bureau packages this information through their

Local Employment Dynamics program and makes available said data on its website. Here at the Department of Workforce

Services, we recently downloaded and packaged Utah-specific data from said

website and summarized it in the attached visualization.

Various data “tabs” are available, presenting Utah’s economy

from different angles, ranging from industry shares within the economy to the

age-group distributions of the labor force, to gender and race distributions.

These labor variables can be viewed for the state as a whole, or by each individual

county.

Some statewide highlights:

Industry — industrial distribution is quite diverse, which

provides strength within the economy. Distributions do fluctuate with time,

with manufacturing seeing its share lessen while health care and professional

and business services shares have increased.

Age — the bulk of Utah’s labor force is composed of 25- to

44-year-olds. Older worker shares have increased over the past 15 years, yet

still remain a non-dominant portion of Utah’s labor force. The youngest segments

of the labor force declined noticeably during the Great Recession due to less

participation, and that trend remains.

Educational Attainment — turnover rates are understandably

highest with workers under the age of 25 as they strive to build their educational

foundation and also find their niche in the labor market. A trend does stand

out where the more education that a worker attains, the lower the turnover rate

businesses experience from said educational classes.

Race/Ethnicity — Whites account for around 80 percent of

Utah’s labor force. The Asian community is small but slowly increasing in

share, and is also characterized with the lowest turnover rate and the highest

new-hire wages.

Gender — males comprise about 55 percent of Utah’s labor

force. The female share of 45 percent is higher than the national average.

Roughly 35 percent of working females work part-time compared to 15 percent for

males. Therefore, female new-hire wages are considerably lower than male

new-hire wages. (Note: employer reporting into the unemployment insurance

system is not hourly wage rate reporting but instead total calendar quarter

wages paid. Therefore, calculations can only be made upon total quarterly

wages, and part-time employment weakens this measure).

As for the various counties in the Bear River region, here

are some labor highlights:

Cache County –

People are often surprised to learn that manufacturing is

the largest sector in Cache County. With Utah State University in Logan, it is

often assumed that education would dominate, but in fact manufacturing composes

about 21 percent of employment while education is about 13 percent. Food product

manufacturing is the largest sub-industry with nearly 4,000 employees

represented by companies like E.A. Miller, Gossner, and Schreiber.

Health care/social services is the only sector that has

substantially increased its share of employment over the last 15 years (the

bump in manufacturing in 2006 was due to a classification change from professional/business

services). Since 2000, the share of employment in health care/social services

has almost doubled from around 6 percent to nearly 11 percent – that’s an

increase of 2,300 jobs. Growth in this sector has been shared across ambulatory

health care as well as hospitals, but the fastest growth has been in residential

intellectual and developmental disability facilities.

Box Elder County –

Manufacturing is an even bigger driver of the economy in Box

Elder County than it is in Cache County. Despite an employment share that has

declined from 46 percent to 29 percent over the last 15 years, it is still by

far the most dominant sector. Over the years, job losses at ATK, and La-Z-Boy

among others, have resulted in the declining share of manufacturing jobs; but

overall, manufacturing employment has been rebounding since the end of the

recession and is back up to nearly 6,000. Autoliv, Thiokol, West Liberty Foods,

and Nucor Steel are just few examples of major manufacturing employers in Box

Elder County.

Like the rest of Northern Utah, the health care/social services

sector in Box Elder has seen notable gains in its employment share over the

last 15 years. Individual and family social assistance services in particular

have grown quickly — more than 100 new jobs just in the last four years.

Rich County –

Not surprisingly, leisure/hospitality services is the

dominant sector in Rich County with about 26 percent of employment, which has remained

relatively consistent across the last 15 years. In that same time, the education

sector has declined from around 20 percent to around 14 percent. In fact, the

actual level of employment in education (which is primarily public schools in

Rich County) has fallen from about 120 in 2000 to about 100 in 2015. Meanwhile,

public administration has gained about 20 jobs over the same period, so its

share has increased to nearly 10 percent.

Wednesday, October 19, 2016

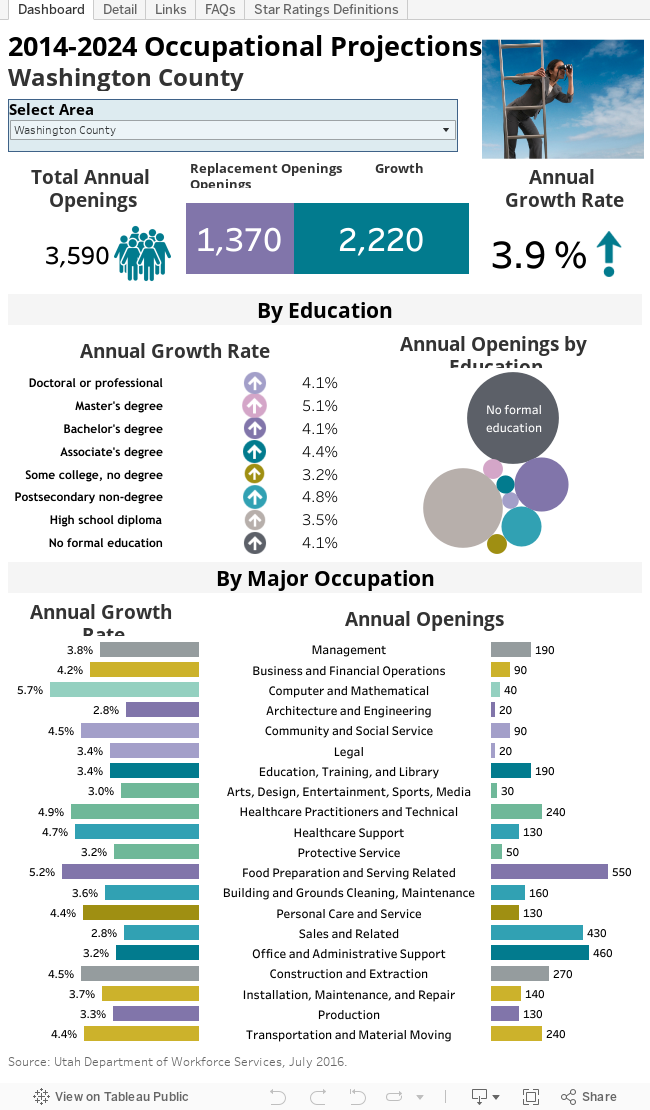

Show Me the Economy - Occupational Projections for Cache County, Utah

The biennial update to Utah's occupational projections have been released and can be found here: http://www.jobs.utah.gov/wi/pubs/outlooks/state/index.html. But first. check out these highlights:

The biennial update to Utah's occupational projections have been released and can be found here: http://www.jobs.utah.gov/wi/pubs/outlooks/state/index.html. But first. check out these highlights:

Cache County Highlights

Matt

Schroeder, Regional Economist

The

projected occupational growth rate in Cache County is slightly below the rest

of the state on average at 2.3 percent annually through 2024. Utah statewide

projected growth is 2.7 percent. The 2,530 projected annual openings in Cache

County from 2014 to 2024 represent about 4 percent of all projected openings in

the state.

The occupations

with the highest growth expectations are, on average, those that require the

most education. Jobs that typically require a doctoral or professional degree

are projected to grow 2.7 percent annually through 2024. Growth in openings for

physicians, physical therapists and psychologists are driving this trend.

Expectations

for healthcare practitioners and healthcare support occupations in Cache County

are worth highlighting. The healthcare industry is supplying large numbers of

annual openings and is expected to grow at more than 3 percent every year over

the next eight years. Registered nurses have the strongest demand outlook among

healthcare jobs, with expected growth of 3.7 percent or about 40 openings a

year, and they earn median wages of nearly $58K per year. Nursing, medical and

dental assistants are also expected to be in demand with about 60 openings per

year combined. These jobs offer median wages between $22K and $28K per year,

but require less education.

After

registered nurses, perhaps the most noteworthy occupations in terms of expected

demand and wages are applications software developers, mechanical engineers and

accountants/auditors. Jobs such as these in the areas of business/finance,

engineering and information technology, tend to offer high wages for the level

of education required and consistently exhibit a strong growth outlook. Application

software engineers are projected to grow by about 3.2 percent or 20 openings

per year in Cache County. They typically require a bachelor’s degree and earn

median wages of $69K per year. Similarly, accountants and auditors are

projected to grow by about 3.2 percent or 20 openings annually and earn median

wages of $55K per year.

There are

many other occupations in the region that are projected to offer excellent

opportunities as well — electrical engineers, mechanical engineers, engineering

techs, cement masons and concrete finishers, environmental science techs, and

management analysts just to name a few. You can learn more about these

occupations and others through the Utah Occupational Explorer

where you can explore and compare occupations of interest in detail by region,

wage level, typical education required, projected growth, and demand. Before

digging into the details though, take a look at the interactive data visualization above to see the big picture of the occupational outlook for Cache County.

About Utah's Occupational Projections

While a Utah

statewide profile leads the way, Utah’s local economies are not homogenous;

therefore, nine Utah subregions are also profiled. Due to confidentiality

restraints and statistical reliability, the amount of occupations available

will diminish the smaller a subregion; but, occupations comprising the backbone

of a regional economy will be available.

About Utah's Occupational Projections

Mark Knold,

Supervising Economist

“The

government knows everything about everyone.”

Fortunately,

that statement is not true. Yet society still looks to the government to

provide answers to comprehensive and complex questions that have their

foundation within individual decisions and activities. One subject frequently

directed toward the government is individual-level information about the

economy — particularly, what occupations are in demand, what occupations pay well

and have lucrative outlooks, and ultimately, what occupation(s) should I build

my career upon?

It takes the

accumulation of a wide array of individual information to answer these

questions. Employers provide the foundation information about the occupations

they employ. Jobs are held by individuals, but employers provide the profile

information about the job itself, not any particular individual.

Since

society desires to profile such a broad spectrum of the economy — occupational

profiles and the occupational distribution within the economy — only government

is in the unique position to collect, analyze and provide answers for said

desire. Yet, no government program or regulatory agency mandates any

comprehensive occupational reporting from individuals or businesses. Therefore,

government attempts to fill the void with an ongoing, robust and voluntary

survey of employers — a survey where employers are asked to provide details

about their various occupations, including descriptions, quantities,

wages/salaries and location. Through this survey emerges an occupational

portrait of an economy.

The U.S.

Bureau of Labor Statistics (BLS) structures and funds the survey, yet the

individual states conduct the survey. Under BLS administration, all states use

the same methodology; therefore, occupational profiles are comparable across

states.

Through this

survey, analysts discover how industries are populated with various

occupations. Accountant is an occupation, yet accountants can be found across

many different industries. Other occupations may be more exclusive to certain

industries; for example, doctors are largely found only in the healthcare

industry. One of the survey’s products is that industries can be profiled with

their general mix of occupations. This is called an industry’s occupational

staffing pattern.

This brings

us back to the original questions: what occupations are in demand, what

occupations pay well and have lucrative outlooks, and ultimately, what

occupation(s) should I build my career upon?

The

foundation is to make informed forecasts about how industries will

expand/contract over the next 10 years. By applying existing occupational

staffing patterns to each industry’s projected change, a trained economic

analyst can then make an extrapolation about how occupations will

correspondingly increase/decrease. Knowledgeable analyst judgment further

refines the occupational expectations, such as knowing an occupation will grow

faster than in the past, with the result being a set of occupational projections

that accumulate to profile a state or regional economy.

A new set of

occupational projections are done every two years to keep the information fresh

even though economies do not change dramatically in short order. Because of

slow change, updated occupational projects generally continue the overall

message of preceding occupational projections. But economies do modify with

time, and therefore, subtle changes will arise with each new set of

occupational projections.

Utah’s most

recent occupational projections are found here: http://www.jobs.utah.gov/wi/pubs/outlooks/state/index.html.

These projections look forward to the year 2024.

The

occupational profile is structured from the general to the detailed, mimicking

the structure of a family tree. First, broad occupational categories are

defined, such as management or healthcare occupations; then, subcategories are

defined; and finally, individual occupations are defined. Individual occupations

are the heart of the occupational projections. But overall patterns and

characteristics do emerge when observing the broader categories.

Wednesday, April 20, 2016

Your area’s labor market information is “OnTheMap”

The Census Bureau’s online mapping tool provides a wealth of

location-specific labor market information

“If you want to put yourself on the map,

publish your own map.” Ashleigh Brilliant

This isn’t your same old blog

post about data. Instead of analyzing and sharing data, this post covers how to

access an extremely useful “big data” labor market information tool. What is

this tool? The U.S. Census Bureau’s OnTheMap web-based mapping and reporting

application.

What’s so great about

OnTheMap? Typically, we report labor market information at the state and county

level. Local-level data is harder to come by. Along with the ability to provide

labor market profiles of small and large nonstandard areas, OnTheMap

graphically demonstrates where people work and where workers live. Users can

define their own geographies and obtain data and maps at the census-block level

of detail. This flexibility can quickly provide information for emergency and

transportation planning, site location and economic development.

- Do you want to understand commuting patterns for a particular area? OnTheMap can generate maps of outflow and inflow.

- Do you want to know the basic characteristics of workers in your town? OnTheMap has that information.

- Do you want to identify the employment characteristics along a specific stretch of highway? OnTheMap can deliver that data.

- Do you want to discern how many workers live within a 50-mile radius of a particular site? OnTheMap delivers.

Where does this data come

from? OnTheMap combines federal and state administrative data on workers and

employees with Census Bureau census and survey data. Don’t worry. Using

state-of-the-art methods, the Census Bureau is committed to protecting the

confidentiality of business and personal information.

Where People Work

Let’s run through a few

examples of how OnTheMap outputs can help you understand your local economy. Suppose

the Logan City Council wants to know where the residents of their town work.

OnTheMap indicates more than half of the city’s working residents are employed in

cities other than Logan.

Next, the mayor wants to know

how many workers travel into Logan for employment. OnTheMap suggests that far more

workers commute in than out of Logan. In-commuters are most likely to drive

from Smithfield.

Labor Market Characteristics

Now, these local government

officials have decided they would like to know the characteristics of those

folks that work or live in Logan. OnTheMap can provide age-group, earnings,

industry, race/ethnicity, gender and educational attainment information. For

example, OnTheMap shows the following characteristics for working residents of

Logan:

- 40 percent are 29 years or younger

- One-fourth make more than $3,333 a month

- 21 percent work in manufacturing

- 1,982 are Latino

- 18 percent have at least a Bachelor’s degree

- 46 percent are female

Getting Specific

A company thinking of

locating to Logan is interested in the number (and characteristics) of workers

within a standard commuting distance of a particular worksite. Economic

development professionals can specify a particular radius and obtain a report.

Other shapes (donut and plume) are also available. In addition, users can draw

their own polygons in OnTheMap. To determine how many workers may be

inconvenienced by a road construction project, just draw a line along the

length of the project and “buffer” the selection.

You begin to see what a

valuable informational tool OnTheMap can be for planning and economic

development purposes.

OnTheMap is available here: http://onthemap.ces.census.gov

Subscribe to:

Posts (Atom)